NHDP vs. Traditional Homebuyer Program: Which One is Right for You?

- Houston Land Bank

- Jan 17

- 7 min read

Buying a home in Houston is a major life goal. However, rising prices can make it feel impossible. The Houston Land Bank exists to solve this problem. They take vacant land and turn it into brand new affordable homes. When you look at their available homes, you will see two main paths. These are the New Home Development Program (NHDP) and the Traditional Homebuyer Program.

Choosing between them can be confusing. You might see terms like "80% AMI" or "Tier 1" and feel lost. It is vital to pick the right lane because each program has different rules about how much money you can make and how much money you can have in the bank. This guide will compare NHDP vs Traditional Homebuyer Program to help you decide which one fits your specific situation.

Key Takeaways

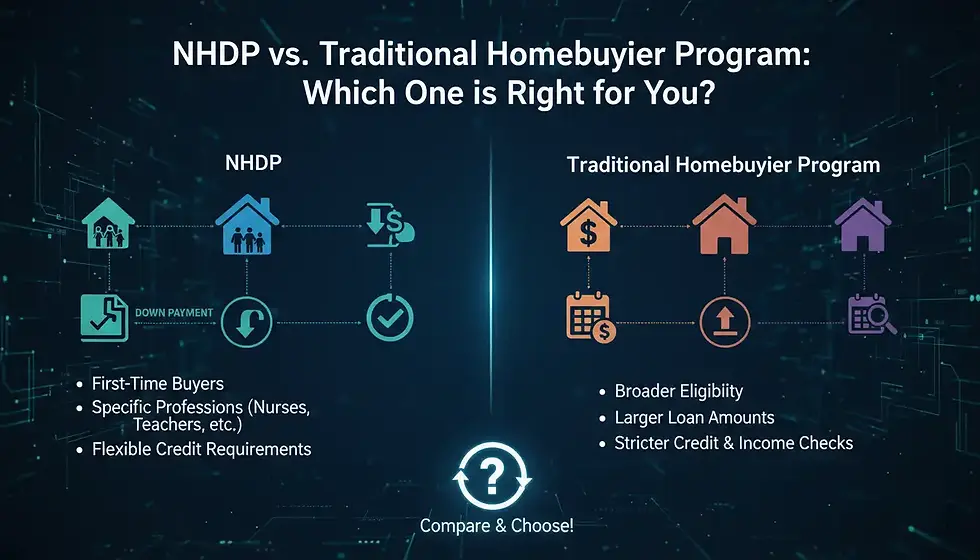

Income Is the Main Factor: NHDP is for households earning up to 80% of the area median income. The Traditional program goes up to 120%.

NHDP Offers More Financial Aid: You could get up to $50,000 in assistance with the NHDP path.

Asset Limits Matter: If you have more than $30,000 in liquid savings, you may not qualify for the NHDP.

Traditional Offers Flexibility: This path is great for moderate-income earners who have some savings but still need a lower home price.

Both Require You to Live There: You must live in the home as your primary residence for both programs.

What is the New Home Development Program (NHDP)?

The New Home Development Program, or NHDP, is the heart of the Houston Land Bank affordable housing program. It is designed for buyers who need the most help to afford a home. This program is a partnership between the Land Bank and the City of Houston.

Who Is It For?

This program is perfect for working-class families and individuals. Think of teachers, medical assistants, retail managers, or retirees on a fixed income. If your income is considered "low" compared to the rest of the region, this is the program for you.

Income Rules (80% AMI)

To qualify, your total household income must be at or below 80% of the Area Median Income (AMI). For a single person in Houston, this might be around $56,000 a year. For a family of four, the limit is higher. If you earn less than these caps, you are in the right place.

The Asset Limit

This is a very important rule. The NHDP has a strict limit on how much cash you can have. You generally cannot have more than $30,000 in liquid assets. Liquid assets include checking accounts, savings accounts, and stocks. This rule exists to make sure the help

goes to people who truly cannot afford a down payment on their own.

The Big Benefit: The $50,000 First-Time Home Buyer Grant

The biggest advantage of the NHDP is the subsidy. Because you are in a lower income bracket, the City of Houston may provide up to $50,000 in assistance. This money acts like a massive down payment. It lowers the amount you need to borrow from the bank. This makes your monthly mortgage payment much lower.

Partnership with Houston Land Trust

Many homes in the NHDP are also part of the Houston Land Trust. This is a special arrangement where you own the house, but the Trust owns the land underneath it. This lowers your property taxes significantly. It ensures you can afford to stay in your home even if property values in the neighborhood go up.

What is the Traditional Homebuyer Program?

The Traditional Homebuyer Program is different. It is designed for the "missing middle." These are people who earn too much to qualify for low-income grants but still cannot afford a $400,000 house on the open market.

Who Is It For?

This path serves moderate-income professionals. You might be a nurse, a police officer, a firefighter, or an office administrator. You have a steady job and good credit, but saving for a

huge down payment is hard.

Income Rules (120% AMI)

The income limits here are much higher. You can earn up to 120% of the Area Median Income. For a single person, this could be upwards of $84,000. This flexibility allows many middle-class families to buy a brand new home in the city.

Asset Rules

The Traditional program is usually less strict about your savings than the NHDP. If you have been saving for years and have more than $30,000 in the bank, you will likely be pushed toward this program. You are expected to contribute more of your own money toward the purchase.

The Benefit: A Discounted Home Price

You might not get the $50,000 first-time home buyer grant with this program, but you still save money. The Houston Land Bank sells the lot to the builder at a discount. In exchange, the builder sells the house to you at a capped price. This means you might buy a home for $250,000 that would cost $350,000 if it were sold by a regular developer. You get instant equity the day you move in.

Side-by-Side Comparison (The Cheat Sheet)

Seeing the facts side-by-side helps makes the choice clearer. Here is how the two programs stack up against each other.

Income Limit

NHDP: Strictly capped at 80% AMI.

Traditional: Goes up to 120% AMI.

Liquid Asset Limit (Savings)

NHDP: Capped at $30,000. You cannot have excessive cash.

Traditional: Limits are higher or determined by the lender.

Financial Assistance

NHDP: Eligible for deep subsidies (up to $50k) from the city.

Traditional: Benefit comes from a reduced sales price, not a direct cash grant.

Property Taxes

NHDP: Often paired with the Community Land Trust for lower taxes.

Traditional: You pay standard property taxes on the full value of the home.

Deed Restrictions

NHDP: You must live there. You cannot rent it out.

Traditional: You must live there. You cannot rent it out.

How to Choose the Right Path

You do not always get to pick. Your financial situation usually decides for you. Here is a simple checklist to see where you fit.

1. Check Your Income

Look at your gross annual income. If you are a single person making $45,000, you are definitely in the NHDP lane. If you make $75,000, you are likely in the Traditional lane. You should look at the "What is AMI" chart to be sure.

2. Assess Your Savings

Open your banking app. Do you have $50,000 sitting in savings? If yes, you are likely ineligible for the NHDP. The program requires you to use your own resources first. The Traditional program is a better fit for buyers with strong savings.

3. Consider Your Needs

Do you need the Harvey Homebuyer Assistance Program or other specific city funds? Often, these funds are tied to specific income levels. If you need maximum cash to close the deal, you should aim for homes designated for NHDP.

4. Location Matters

Some neighborhoods have more NHDP homes, while others have more Traditional homes. It depends on what the Land Bank has built in that area. However, you should never try to fit into a program you do not qualify for just to get a specific house. The rules are strict.

Other Assistance Programs You Should Know

The Houston Land Bank is not the only group helping people. There are other programs that can sometimes work together with your purchase.

Harris County Homeowner Assistance Program

If you are looking outside the city limits or in specific areas, the Harris County homeowner assistance program helps with down payments. It is worth checking if you can layer this assistance, though rules vary by property.

Houston Assistance Programs

There are many Houston assistance programs designed to help with closing costs. Even if you are in the Traditional program, you might qualify for smaller grants of $5,000 or $10,000 from private banks or state agencies. Always ask your loan officer about "DPA" (Down Payment Assistance).

The Houston Land Trust

We mentioned this earlier, but it is key. The Houston Land Trust is a separate tool often used with NHDP. It permanently lowers the cost of the home. It protects you from gentrification. If taxes in your area double next year, your taxes stay low because the Trust owns the land.

Frequently Asked Questions (FAQs)

What are the advantages of the HBP?

The main advantage of the Homebuyer Program (HBP) through the Land Bank is instant equity. You are buying a new construction home for less than it cost to build. You also get a stabilized mortgage payment that will not go up like rent does.

What's the best type of mortgage for first time buyers?

For these programs, a 30-year fixed-rate mortgage is strongly recommended. In fact, the Houston Land Bank usually requires it. They do not allow risky loans like Adjustable Rate Mortgages (ARMs). This protects you from payment spikes in the future.

Are there any benefits of being a first-time buyer?

Yes. Most of the grant money, including the $50,000 first-time home buyer grant, is reserved for people who have not owned a home in the last three years. Being a first-time buyer opens the door to free money that you do not have to pay back as long as you live in the house.

Can I rent out the home later?

No. Both NHDP vs Traditional Homebuyer Program rules state that you must be an owner-occupant. These homes are for people to live in, not for investors to make money on. If you move out, you may have to sell the home to another qualified low-income buyer.

Final Words

Deciding between the NHDP and the Traditional Homebuyer Program comes down to the numbers. It is not about which one is "better." It is about which one fits your life.

If you are working hard but your income is low, the NHDP is a lifeline. It gives you the cash and the price break you need to stop renting. If you are earning a moderate income and want a quality new home at a fair price, the Traditional program is your answer.

The first step is to get your paperwork ready. Gather your pay stubs and check your savings. Once you know your numbers, you can look at the New Home Development Program and Traditional listings with confidence. Do not wait. These homes sell fast. Contact a Land Bank approved lender today to get pre-qualified and start your journey home.

Comments